Corporate governance status

① Overview of corporate governance system

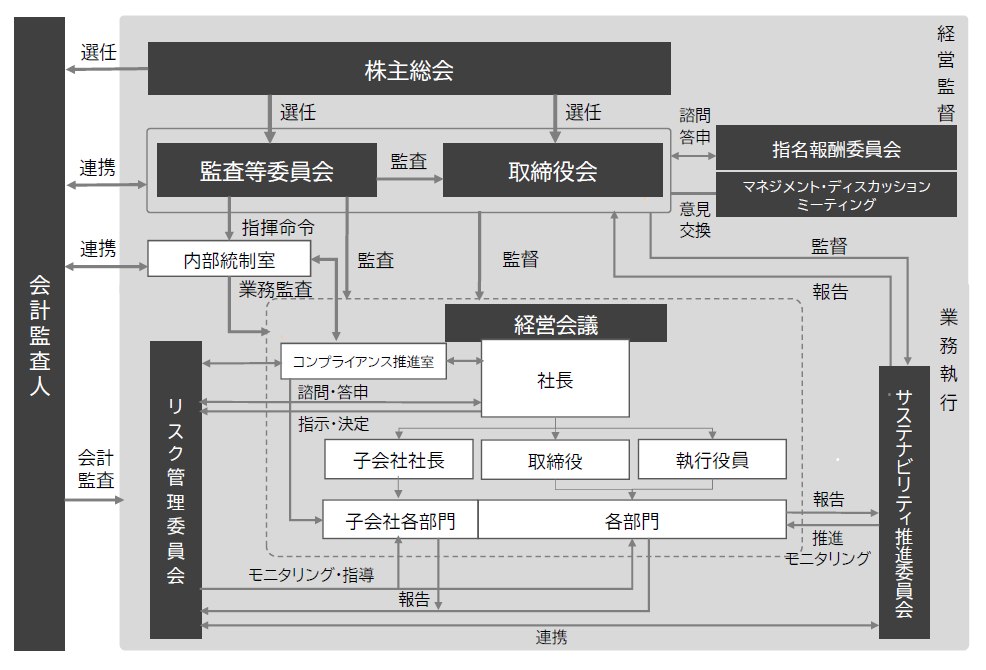

I. Overview of corporate governance system

In addition to the Board of Directors, which meets once a month in principle, the Company has established meeting bodies such as the Management Committee, which are not required to be established by law, to conduct flexible and thorough deliberations according to the importance and urgency of each issue. The Company has also established the Nomination and Remuneration Committee and the Management Discussion Meeting as advisory bodies to the Board of Directors.

The Nomination and Compensation Committee is composed of directors, the majority of whom are Independent Director, and is chaired by an independent Independent Director. It will consider matters relating to the appointment and dismissal of directors and executive officers of the Company and its subsidiaries, as well as succession plans and compensation.

The Management Discussion Meeting is comprised of Independent Director and the representative director and provides a forum for the exchange of opinions regarding important management issues.

In addition, the Audit and Supervisory Committee conducts rigorous audits of the decision-making of the Board of Directors and the execution of duties by the directors, and cooperates with the Internal Audit Department by receiving timely reports, etc. By adopting the above system, we strive to strengthen governance throughout the Group, achieve sustainable growth for the Company, and increase corporate value over the medium to long term.B. Why adopt corporate governance?

当企業グループが掲げる「サービス型小売業」は、株主様、お客様、お取引先様、地域社会というステークホルダーからいただく安心と信頼のもとに成り立つ地域密着型の小売業であります。

競争と変化の激しい経営環境の中で発展を続けるとともに、「サービス型小売業」として地域社会に受け入れられ、広くご支持をいただくためには、当企業グループ内のガバナンスが重要な経営課題であると認識しております。適切な権限委譲により迅速かつ的確な意思決定が行われるとともに、重要事項については取締役会での審議・決議に基づく業務執行を行うトップマネジメント体制を構築し、併せて現場情報とステークホルダーのご意見・ご要望が迅速に取締役に伝達されるよう社内コミュニケーションの向上に絶えず努めております。

また、当企業グループとステークホルダーとの良好な関係づくりが重要な経営課題であると認識しております。そのため各ステークホルダーから見た経営施策の合理性・納得性と意思決定プロセスの透明性を確保するとともに、各ステークホルダーに向けた説明責任を十分に果たします。

さらに、お客様にご信頼をいただくための前提として、役員・社員のコンプライアンス(法令遵守)徹底に向けた組織的対応も欠かすことはできません。当企業グループではこれらをすべて併せてコーポレート・ガバナンスの課題としてとらえております。

また、取締役又は執行役員が本部長を務めることによって、経営上の課題等を迅速かつ的確に把握し、管理機能の強化と各営業店舗までの迅速な経営意思の徹底を図ります。また、関係会社管理規程に従い、各子会社の独自性・特性を踏まえつつ、エディオングループとしての基本的ルールを遵守させるとともに、グループ間での人材交流を図りコミュニケーションを活性化することで、グループ全体としての意思統一を図っております。

以上の体制を適切に運用するとともに、適宜見直しを行うことで、今後とも一層のコーポレート・ガバナンスの強化・充実を図ってまいりります。C. Status of improvement of internal control system and risk management system

The following figure shows a schematic diagram of the state of the main group, internal control system and risk management system in the Group.

- D. Summary of the contents of the liability limitation agreement and directors and officers liability insurance (D&O insurance) and the reasons for it

The Articles of Incorporation provide that the Company may be exempted from such liability by a resolution of the Board of Directors. In addition, the Articles of Incorporation provide that the Company may enter into agreements with directors, excluding executive directors, etc., to limit the liability for damages under Article 423, Paragraph 1 of the Companies Act, pursuant to the provisions of Article 427, Paragraph 1 of the Companies Act.

Pursuant to Article 427, Paragraph 1 of the Companies Act, the Company has entered into agreements with one full-time director who is an audit and supervisory committee member and eight Independent Director to limit the liability for damages under Article 423, Paragraph 1 of the Companies Act, and the amount of such liability is set at the minimum liability limit prescribed by law.

In addition, the Company has entered into a Company Officer Liability Insurance contract with its directors and directors (audit and supervisory committee members) and its subsidiaries' directors and auditors as insured persons. The outline of the contents of the contract is to compensate the insured for damages, litigation costs, etc. incurred by the insured when a claim for damages is made due to the insured's acts in the course of their duties as a company officer. The insurance premiums are paid in full by the Company.

These are intended to enable directors to fully fulfill the roles expected of them in carrying out their duties. E. Number of directors

Our Articles of Incorporation stipulate that the number of directors excluding directors who are audit and supervisory committee members shall be 16 or less, and the number of directors who are audit and supervisory committee members shall be 5 or less.

What. Requirements for resolution of appointment of directors

Regarding the resolution for the election of directors, we state that shareholders who have one-third or more of the voting rights of the shareholders who can exercise their voting rights shall attend, and that the majority of the voting rights shall be adopted and that cumulative voting shall not be used. It is stipulated in the articles of incorporation.

G. Acquisition of own shares

Regarding the acquisition of own shares, the Articles of Incorporation stipulate in Articles 165, Paragraph 2 of the Companies Act that the Company's own shares may be acquired through market transactions, etc. by resolution of the Board of Directors. This is intended to enable flexible execution of capital policies.

blood. Interim dividend

Pursuant to the provisions of Article 454, Paragraph 5 of the Companies Act, the Company may pay an interim dividend to shareholders or registered share pledgees recorded in the final shareholder list on September 30 every year by a resolution of the Board of Directors. The articles of incorporation stipulate that to that effect. The purpose of this is to provide stable and agile return of profits to shareholders.Li. Special resolution requirements for general meetings of shareholders

At the Company, shareholders who hold one-third or more of the voting rights of shareholders who can exercise their voting rights attend the special resolution of the general meeting of shareholders stipulated in Article 309, Paragraph 2 of the Companies Act, and the voting rights 3 It is stipulated in the Articles of Incorporation that a majority, which is more than two-minutes, will be used. The purpose of this is to facilitate the operation of the general meeting of shareholders by relaxing the quorum of special resolutions at the general meeting of shareholders.

② Status of audits by the Audit and Supervisory Committee and internal audits

A. Status of audits by the Audit and Supervisory Committee

(1) Organization and personnel of the Audit and Supervisory Committee

監査等委員会は、公認会計士、企業経営・財務等、弁護士の専門的知見を有した独立社外取締役3名を含む監査等委員である取締役4名(男性3名、女性1名)で構成しております。

当事業年度においては、監査等委員である社外取締役坂井義清氏が監査等委員会委員長を務めております。同氏は通信ネットワーク事業を営む企業の財務経理部門担当及び業務執行取締役としての豊富な実務経験を有し、財務会計及び税務に関する相当程度の知見を有しております。

監査等委員である社外取締役の福田有希氏は公認会計士及び税理士の資格を有し、財務会計及び税務に関する相当程度の知見を有しております。

監査等委員である社外取締役の清水英昭氏は弁護士としての企業法務の経験と専門的知見から、経営の監査及び監督を行うに十分な見識を有しております。

常勤監査等委員である取締役の山根よしえ氏は、当社や子会社の管理部門での豊富な経験から、情報収集の充実を図り、内部監査部門(内部統制室)との十分な連携を通じて監査体制に必要な業務知識を幅広く有しております。

加えて、監査等委員会は監査等委員の職務を補助する体制として、監査等委員会事務局を設置し、専任のスタッフを配置して、情報収集の指示や事務局としての会議運営、監査等委員間の連絡調整業務等、監査等委員会の職務執行に必要な事項を補助しております。

(2) Activities of the Audit and Supervisory Committee

当事業年度においては、監査等委員会を14回開催し、監査等委員である取締役4名はその全てに出席いたしました。当事業年度における監査等委員会で審議・決議した主な議案内容以下のとおりです。

・Audit report of the Board of Auditors for the previous fiscal year

- Consent regarding the estimated audit fees of the accounting auditor

・Selection of the Chairman of the Audit and Supervisory Committee, full-time Audit and Supervisory Committee members, and selected Audit and Supervisory Committee members

・Establishment of rules for the Audit and Supervisory Committee

・Establishment of standards for audit and supervisory committee audits and implementation standards for audit and supervisory committee audits related to internal control systems

・Basic audit policy of the Audit and Supervisory Committee ・Audit implementation plan ・Division of audit duties

・Remuneration for directors who are audit and supervisory committee members (discussion)

- Whether or not to reappoint the accounting auditor based on the evaluation

・Opinions regarding the appointment, etc. of directors (excluding directors who are audit and supervisory committee members) and remuneration, etc.

・Approval of transactions that may involve a conflict of interest for directors

- Annual audit plan of the accounting auditor

-Evaluation of the suitability of accounting auditors

・Matters to be discussed by the business execution division

・Audit report from accounting auditor

・Internal audit plans and audit result reports from the Internal Control Office

・Audit activity report from the full-time audit and supervisory committee member

With regard to the "Key Audit Matters" (KAMs) stated in the accounting auditor's audit report based on the Financial Instruments and Exchange Act, the accounting auditor and the Audit and Supervisory Committee held repeated discussions in cooperation with the executive department throughout the fiscal year, and confirmed the appropriateness and consistency of information disclosure on items involving important management judgment, including accounting estimates. In addition, twice a year, EDION Group Audit Liaison Conference was held, bringing together the accounting auditor, the Audit and Supervisory Committee members, the Internal Control Office, the Finance and Accounting Department, and the auditors of subsidiaries, where the accounting auditor explained the audit results, a question-and-answer session was held, and opinions were exchanged to share current issues.

(3)監査等委員である取締役の活動内容

当社の監査等委員である取締役は、監査等委員会で定めた監査の基本方針、監査の実施計画、監査職務の業務分担等に従い監査を行っております。主な活動は以下のとおりです。

・代表取締役をはじめとした業務執行取締役との意見交換会を開催し、リスクの高い経営課題について提言を行いました。

・サステナビリティ監査においては、当社のマテリアリティの推進状況や、気候変動への対応などをサステナビリティ推進部門の責任者へヒアリングを行い、サステナビリティ経営の監査を行いました。常勤監査等委員である取締役はサステナビリティ推進委員会へ委員として参画し、マテリアリティの見直し等の審議状況を監査し適宜意見を表明しております。

・監査等委員である社外取締役は、取締役会、経営方針発表会への出席、重要な事業所の視察等を通じて、取締役及び使用人等の職務の執行状況を監査しました。また、取締役会の諮問機関である任意の指名報酬委員会に委員として出席する監査等委員である社外取締役は、取締役(監査等委員である取締役を除く。)の選任等及び報酬等の審議・決定プロセスの妥当性を監査しております。

・常勤監査等委員である取締役は、日々の監査活動において業務執行取締役、内部統制室その他の使用人等と意思疎通を図り、情報の収集及び監査の環境の整備に努めるとともに、経営会議、賞罰委員会、リスク管理委員会等重要な会議に出席し、業務執行取締役及び使用人等からその職務の執行状況について報告を受け、必要に応じて説明を求め、重要な決裁書類等を閲覧しました。加えて、本社及び主要な店舗において内部統制室の往査に同行し業務及び財産の状況を監査しました。さらに会計監査人の内部統制監査に同行して主要な店舗に赴き、監査の方法と結果が相当であるかを監査しました。これらの監査活動及び監査結果は、常勤監査等委員である取締役が監査等委員会で適宜報告しております。

・子会社については、常勤監査等委員である取締役がその非常勤監査役を兼務する子会社にあっては取締役会に出席するほか、その他の子会社を含め、内部統制室又は会計監査人の往査に同行し、子会社の取締役及び監査役等と意思疎通及び情報交換を図り、必要に応じて子会社から事業の報告を受けるとともに、リスク管理体制について監査しました。

・当事業年度における監査等委員会の活動状況等は、定期的に取締役会で報告しております。

B. Status of internal audits

当社の内部監査は、会社の組織、制度及び業務が経営方針及び諸規程に準拠し、効率的に運用されているかを検証、評価及び助言することにより、不正、誤謬の未然防止、正確な管理情報の提供、財産の保全、業務活動の改善向上を図り、経営効率の増進に資することを目的としております。

代表取締役会長執行役員直属で業務執行部門から独立した組織の内部統制室(本報告書提出日現在29名)が年間内部監査計画に基づき、営業店舗、物流サービス拠点、本社部署及び子会社の監査を実施しております。各部門の業務執行状況について法令、社内規程、諸取扱要領に従って適正かつ有効に運用されているかを監査し、その監査結果は被監査部門に通知し、業務改善及び不正や誤謬の防止についての助言を行い、適切なフォローアップを通じて実効性の強化を図っております。内部統制室は取締役会、監査等委員会が必要と認めた事項についての監査及び金融商品取引法に基づく財務報告に係る内部統制の整備及び運用状況の評価も実施しております。

内部監査の結果及び内部統制評価の結果につきましては、代表取締役会長執行役員のみならず、取締役会、監査等委員会においても直接報告しております。

内部統制室は、監査等委員である取締役及び監査等委員会並びに会計監査人と定期的又は必要に応じて報告や情報交換を行い、相互連携の強化を図っております。また、内部統制室長は、当連結会計年度に開催されたすべてのエディオングループ監査等連絡会議やリスク管理委員会へ出席し、当社及び子会社のリスク案件等の情報連携を図り、改善対策に努めております。

C. Status of accounting audit

当社は、会社法に基づく会計監査人及び金融商品取引法に基づく会計監査をEY新日本有限責任監査法人に委嘱しておりますが、同監査法人及び当社監査に従事する同監査法人の業務執行社員と当社の間には、特別の利害関係はありません。また、法定監査はもとより、監査等委員会及び内部統制室との間で、監査報告をはじめ、意見交換等を定期的に実施しております。

Name of the audit firm

EY ShinNihon LLC

b.業務を執行した公認会計士

指定有限責任社員 業務執行社員 諏訪部修

指定有限責任社員 業務執行社員 小林謙一郎

c.監査業務に係る補助者の構成

当社の会計監査業務に係る補助者は、公認会計士9名、その他19名です。

d.監査法人の選定方針と理由

当社では、会計監査人候補を適切に選定し、以下のとおり、外部会計監査人を適切に評価するための基準を設けております。

(1) 品質管理システムについて

・会計監査人の品質管理システムは、毎年会計監査人から品質体制についての報告を受け、適正な監査の確保に向けて適切な対応を行うことができる体制があること

・外部レビュー(公認会計士・監査審査会検査、日本公認会計士協会品質管理レビュー)等で、品質管理システムに影響を与えるような重大な指摘がないこと

(2) 監査計画について

・業界及び会社の環境に則した監査計画を策定していること

・監査計画策定に当たり、監査役からの要望等を反映していること

会計監査人に求められる独立性と専門性を有しているか否かについては、以下3点を基準にして確認しております。

(1) 会計監査人及び監査チームは、公認会計士法等で求められる独立性を保持していること

(2) 監査計画に従った監査を実施する知識及び経験を有したメンバーを監査チームに加えていること

(3) 複雑で重要な専門領域がある場合、会計及び監査以外の専門家を利用していること

これらを踏まえ、会計監査の監査の遂行状況、品質管理体制、独立性及び専門性等を総合的に評価した結果、EY新日本有限責任監査法人の適格性に問題はないと判断し、同監査法人を会計監査人として再任することを決定いたしました。

監査等委員会は、会計監査人が適正に監査を遂行することが困難であると認められるなど、その他必要があると判断した場合には、株主総会に提出する会計監査人の解任又は不再任に関する議案の内容を決定いたします。

また、監査等委員会は、会計監査人が会社法第340条第1項各号に定める事由に該当すると認められる場合は、監査等委員全員の同意により、会計監査人を解任いたします。この場合、監査等委員会が選定した監査等委員は、解任後最初に招集される株主総会において、会計監査人を解任した旨及び解任の理由を報告いたします。

e.監査等委員会による監査法人の評価

監査等委員会は、会計監査人が独立の立場を保持し、かつ、適正な監査を実施しているかを監視及び検証するとともに、会計監査人からその職務の執行状況について報告を受け、必要に応じて説明を求めました。

また、会計監査人から「職務の遂行が適正に行われることを確保するための体制」(会社計算規則第131条各号に掲げる事項)を「監査に関する品質管理基準」(企業会計審議会)等に従って整備している旨の通知を受け、必要に応じて説明を求め、総合的に勘案した結果、会計監査人の職務の執行が適切であると評価いたしました。

③ Independent Director and Auditor

当社の社外取締役は6名、社外取締役(監査等委員)は3名であります。

社外取締役(監査等委員)については、取締役(監査等委員)総数(4名)の過半数及び定款に定められた監

査等委員である取締役の定数(5名以内)を満たしており、現陣容にて充分な監査機能を果たしております。

- A. Personal relationships, capital relationships, business relationships, or other interests between the Company and Independent Director and Independent Director (audit and supervisory committee members)

There are no special interests between the Company and its Independent Director or Independent Director (audit and supervisory committee members) that need to be disclosed. - ロ. 社外取締役及び社外取締役(監査等委員)が他の会社等の役員若しくは使用人である、又は役員若しくは使用人であった場合における当該他の会社等と当社との人的関係、資本的関係又は取引関係その他の利害関係

社外取締役石橋省三氏は、一般財団法人石橋湛山記念財団代表理事、株式会社ミンカブ・ジ・インフォノイド社外取締役、学校法人栗本学園理事をそれぞれ兼職し、過去において株式会社野村総合研究所、野村證券株式会社、リーマン・ブラザーズ証券株式会社、国立大学法人東京医科歯科大学、学校法人立正大学にそれぞれ在籍しておりましたが、当社と当該会社・法人との間に特別の利害関係はありません。

社外取締役髙木施文氏は、髙木法律事務所を開業し、過去においてブレークモア法律事務所、足立・ヘンダーソン・宮武・藤田法律事務所、ベーカー&マッケンジー法律事務所、ホワイト&ケース法律事務所にそれぞれ在籍しておりましたが、当社と当該法人との間に特別の利害関係はありません。

社外取締役眞弓奈穗子氏は、アルゴラブ株式会社代表取締役社長を兼職し、過去において岡三証券株式会社、ドイチェ・アセット・マネジメント株式会社、UBSアセット・マネジメント株式会社、ラザード・ジャパン・アセット・マネージメント株式会社にそれぞれ在籍しておりましたが、当社と当該会社との間に特別の利害関係はありません。

社外取締役福島淑彦氏は、早稲田大学政治経済学術院教授を兼職し、過去においてシティグループ証券株式会社、スウェーデン王立ストックホルム大学、名古屋商科大学にそれぞれ在籍しておりましたが、当社と当該会社・法人との間に特別の利害関係はありません。

社外取締役森忠嗣氏は、株式会社ヒト・コミュニケーションズ・ホールディングス社外取締役、シルバーエッグ・テクノロジー株式会社社外取締役をそれぞれ兼職し、過去において株式会社阪急百貨店、エイチ・ツー・オーリテイリング株式会社、株式会社梅の花、株式会社関西スーパーマーケットにそれぞれ在籍しておりましたが、当社と当該会社との間に特別の利害関係はありません。

社外取締役後藤研二氏は、株式会社Mirai Nihon Ventures代表取締役、株式会社極楽湯ホールディングス取締役、アビスパ福岡株式会社取締役を兼職し、過去において兼松株式会社、日興証券株式会社、伊藤忠商事株式会社、いちごグループホールディングス株式会社、いちご不動産投資顧問株式会社にそれぞれ在籍しておりましたが、当社と当該会社との間に特別の利害関係はありません。

社外取締役(監査等委員)福田有希氏は、福田公認会計士・税理士事務所を開業し、株式会社精工監査役を兼職し、過去においてEY新日本有限責任監査法人に在籍しておりましたが、当社と当該法人との間に特別の利害関係はありません。

社外取締役(監査等委員)坂井義清氏は、NTTファイナンス株式会社相談役を兼職し、過去において株式会社NTTドコモ、東日本電信電話株式会社、日本電信電話株式会社にそれぞれ在籍しておりましたが、当社と当該会社との間に特別の利害関係はありません。

社外取締役(監査等委員)清水英昭氏は、清水英昭法律事務所を開業し、過去において山田忠史法律事務所、上原・清水法律事務所にそれぞれ在籍しておりましたが、当社と当該会社との間に特別の利害関係はありません。 - ハ. 社外取締役及び社外監査役が当社のコーポレート・ガバナンスにおいて果たす機能及び役割

社外取締役石橋省三氏は、企業経営・金融における豊富な経験と知見を有しており、取締役会等における発言や、取締役会の諮問機関である任意の指名報酬委員会の委員長を務めるなど、自らの経験と知見を踏まえた活動を行っております。

社外取締役髙木施文氏は、弁護士としての企業法務の経験と専門的知見を有しており、取締役会等において自らの経験と知見を踏まえた発言を行っております。

社外取締役眞弓奈穗子氏は、金融・証券部門における豊富な経験に基づく助言等、当社の社外取締役として適切に職務を遂行していただいております。

社外取締役福島淑彦氏は、社外役員以外の方法で会社経営に関与したことはありませんが、経済・経営分野における学識者としての知見に基づく助言等、当社の社外取締役として適切に職務を遂行していただいております。

社外取締役森忠嗣氏は、小売業を営む企業の業務執行取締役としての豊富な経験及び知見に基づく助言等、当社の社外取締役として適切に職務を遂行していただいております。

社外取締役後藤研二氏は、金融、商社、不動産等様々な企業の業務執行者又は経営者としての豊富な経験を有しております。

社外取締役(監査等委員)福田有希氏は、公認会計士及び税理士の資格を有しており、財務及び会計に関する相当程度の知見を有するものであります。

社外取締役(監査等委員)坂井義清氏は、通信ネットワーク事業を営む企業の財務経理部門担当及び業務執行取締役としての豊富な経験及び知見に基づき、独立した客観的な立場での提言や助言等、当社の社外取締役として適切に職務を遂行いただいております。

社外取締役(監査等委員)清水英昭氏は、弁護士としての企業法務の経験と専門的知見を有するものであります。 ニ. 社外取締役及び社外監査役の選任状況に関する当社の考え方

当社は、社外取締役及び社外監査役を選任するための基準として、会社法における規定及び証券取引所の「上場管理等に関するガイドライン」を満たすとともに、さらに、以下に定める当社独自の独立性基準を設けております。

なお、社外取締役6名及び社外取締役(監査等委員)3名はいずれも証券取引所の定める独立役員の要件を満たすとともに、また、当社独自の基準を満たしており、独立性は保たれております。< Independence criteria >

Persons who do not meet any of the criteria set out below

a. A person who currently or previously executed business operations for the Company or any of its subsidiaries

- b. An executive officer currently belonging to a major shareholder or an organization that is a major shareholder with a voting rights ratio of 10% or more in the most recent shareholder register of the Company

- c. An executive officer currently working for a business partner or its consolidated subsidiary whose total transaction amount with the Company exceeded 2% of Consolidated net sales of the Company or the business partner at least once during the most recent three fiscal years.

- d. A consultant, accounting professional, legal professional, accounting auditor, or advisory contract partner who has received an average of 10 million yen or more in cash or other assets from the Company in the most recent three fiscal years other than officer compensation (if such a partner is an organization such as a corporation or association, an executive officer of such organization)

- e. A director or other executive officer of an organization that has received donations from the Company in excess of the greater of 10 million yen or 2% of Net sales or total income during the past three fiscal years.

- If you were previously affiliated with any of the organizations or business partners listed in b through e, you have left those organizations or business partners within the past year, and you are the spouse or a relative within the second degree of kinship of the Company or any of the business executives listed in a through e.

- ホ. 社外取締役又は社外取締役(監査等委員)による監督又は監査と内部監査、監査等委員会及び会計監査との相互連携並びに内部統制部門との関係

社外取締役及び社外取締役(監査等委員)は、取締役会に出席し、内部監査の状況、金融商品取引法に基づく内部統制の評価結果、監査等委員会監査の状況等の報告を受けております。

社外取締役(監査等委員)は、監査等委員会において定期的に内部監査部門(内部監査室)及び会計監査人と情報交換を行い、監査計画、監査実施状況及び監査で指摘された問題点等について報告を受けるとともに、監査に関する情報の共有と意見交換を行っております。

④Remuneration of officers

A. Total amount of remuneration for each executive category, total amount by type of remuneration, and number of eligible executives

Officer classification Such as rewards

the amount

(One million yen)Total amount by type of compensation (million yen) Target

Officer's

Number of members (people)Basic

RewardPerformance linked

RewardNon-monetary

RewardDirectors (excluding Audit and Supervisory Committee members and Independent Director) 667

378

212

76

9

Directors (Audit and Supervisory Committee Members) (excluding Independent Director) 14

14

-

-

1

Auditors (excluding outside auditors) 3

3

―

―

1

Outside officer 88

88

―

―

8

(注)1.上記取締役の報酬等の総額には、使用人兼務取締役の使用人分給与は含まれておりません。

2.業績連動報酬等に係る業績指標は、親会社株主に帰属する当期純利益であり、2026年3月期の実績は15,453百万円です。3.取締役(監査等委員及び社外取締役を除く)の報酬等の種類別の額の「非金銭報酬等」は、譲渡制限付株式報酬76百万円です。

B. Total amount of remuneration, etc. of persons whose total amount of remuneration, etc. is 100 million yen or more

Full name Officer classification Company classification Total amount by type of compensation (million yen) Such as rewards

the amount

(One million yen)Basic reward Performance linked

RewardOther Masataka Kubo Director Submission

Company157

102

28

289

髙橋 浩三 Director Submission

Company55

31

14

101

(注)1.久保 允誉に対する報酬等の種類別の額の「非金銭報酬等」は、譲渡制限付株式報酬28百万円です。

2.髙橋 浩三に対する報酬等の種類別の額の「非金銭報酬等」は、譲渡制限付株式報酬14百万円です。

⑤Shareholding status

B. Number of issues and amount on balance sheet

Number of brands (brands) On the balance sheet

Total amount (million yen)Unlisted stock ― ― Non-listed shares 4 4,234

(Issues whose shares decreased during the current fiscal year) Number of brands (brands) Acquisition price related to the increase in the number of shares

Total amount (million yen)Unlisted stock ― ― Non-listed shares ― ― B. Information on the number of shares, balance sheet amounts, etc. for each stock of specific investment shares and deemed holding shares

Specified investment stock Brand This business year Previous business year Holding purpose,

Quantitative

Holding effect and

The number of shares

Reasons for increaseOf our stock

PossessionNumber of shares (shares) Number of shares (shares) Balance sheet

Recorded amount (million yen)Balance sheet

Recorded amount (million yen)㈱ひろぎんホールディングス 1,146,000 1,146,000 Stable

Maintain financial transactionsYes 1,969 1,388 ㈱Mitsubishi UFJ Financial Group 504,420 504,420 Stable

Maintain financial transactionsYes 1,311 1,014 ㈱Sanae 154,400 154,400 Business transactions

(franchised contracts)

Medium to long term

Relationship maintenanceNothing 470 484 Aichi Financial Group Co., Ltd. 70,284 70,284 Stable

Maintain financial transactionsYes 482 200 (Note) If the issue is a holding company, the presence or absence of shares of the Company is stated in consideration of the shares held by its major subsidiaries (the number of shares actually owned).

C. Investment stocks held for pure investment purposes

Classification This business year Previous business year Number of brands (brands) On the balance sheet

Total amount (million yen)Number of brands (brands) On the balance sheet

Total amount (million yen)Unlisted stock 21

2,179

21

2,179

Non-listed shares 4

54

4

43

Classification This business year Dividend income

Total amount (million yen)Of gain or loss on sale

Total amount (million yen)Of valuation loss

Total amount (million yen)Unlisted stock 24

―

(note)-

Non-listed shares 0

-

32

(Note) For unlisted stocks, there is no market price, and it is considered extremely difficult to determine the market value.

Details of audit fees

Remuneration for auditing certified public accountants

a.Remuneration for auditing certified public accountants, etc.

Classification | Previous consolidated fiscal year | Current consolidated fiscal year | ||

|---|---|---|---|---|

| For audit certification work Remuneration (million yen) | For non-audit work Remuneration (million yen) | For audit certification work Remuneration (million yen) | For non-audit work Remuneration (million yen) | |

| Submitting company | 111 | 2 | 118 | 19 |

| Consolidated subsidiary | ― | ― | ― | ― |

| Total | 111 | 2 | 118 | 19 |

(注)前連結会計年度における提出会社の支払った監査証明業務に基づく報酬は、10百万円の追加報酬の額を含んでおります。また、前連結会計年度における提出会社の支払った非監査業務に基づく報酬の内容は、新リース会計への対応に関するアドバイザリー業務であります。当連結会計年度における提出会社の支払った監査証明業務に基づく報酬は、12百万円の追加報酬の額を含んでおります。また、当連結会計年度における提出会社の支払った非監査業務に基づく報酬の内容は、財務情報に係る調査業務であります。

b. Compensation for organizations belonging to the same network (Ernst & Young member firms) as audit certified accountants (excluding a.)

Not applicable.

c. Remuneration for other important audit certification services

Not applicable.

d. Policy for determining audit fees

It is determined after considering the size, characteristics, number of audit days, etc.

e. Reasons for the Board of Corporate Auditors to agree to the remuneration of the Accounting Auditor

監査等委員会は、会計監査人の監査計画、会計監査の職務遂行状況及び報酬見積りの算出根拠等が適切であるかどうかについて必要な検証を行い審議したうえで、会計監査人の報酬等の額は妥当と判断し、会社法第399条第1項及び同条第3項の同意を行っております。

Director Skills Matrix

The main skills and experience possessed by each director, as well as expected roles, etc. are marked with a ●.

Full name | Position | Business Management Business Strategy | Financial Accounting Tax | sales Marketing | Store Development | IT/DX | Logistics Logistics | human resources Human Resources Development | Legal Affairs Risk Management | Internal Control Governance | Sustainer Ability |

|---|---|---|---|---|---|---|---|---|---|---|---|

Masataka Kubo | CEO Chairman, Executive Officer and CEO | ● | ● | ● | ● | ● | ● | ● | |||

Norio Yamazaki | CEO Vice Chairman | ● | ● | ● | ● | ● | ● | ● | |||

Kozo Takahashi | CEO President and COO | ● | ● | ● | ● | ● | ● | ● | |||

Aki Ishida | Director Managing Executive Officer | ● | ● | ● | ● | ● | ● | ● | |||

Toshiro Inoue | Director Senior Executive Officer | ● | ● | ||||||||

Hirokazu Fujiwara | Director Senior Executive Officer | ● | ● | ● | ● | ||||||

Shozo Ishibashi | Independent Director | ● | ● | ● | ● | ||||||

Takagi Shigefumi | Independent Director | ● | ● | ● | ● | ||||||

Mayumi Naoko | Independent Director | ● | ● | ● | ● | ||||||

Yoshihiko Fukushima | Independent Director | ● | ● | ● | ● | ● | |||||

Tadatsugu Mori | Independent Director | ● | ● | ● | ● | ● | |||||

後藤研二 | Independent Director | ● | ● | ● | ● | ||||||

Yoshie Yamane | Director Full-time Audit and Supervisory Committee Member | ● | ● | ● | ● | ● | |||||

Yuki Fukuda | Independent Director Audit and Supervisory Committee Members | ● | ● | ● | |||||||

Yoshikiyo Sakai | Independent Director Audit and Supervisory Committee Members | ● | ● | ● | ● | ● | |||||

Hideaki Shimizu | Independent Director Audit and Supervisory Committee Members | ● | ● |